You do not need to be an accountant to understand your business finances.

Yet many business owners avoid financial reports because they seem too complex, too technical, or too time-consuming.

The truth is simple: if you can understand your numbers, you can control your business.

In this guide, we show you how to prepare financial reports step by step, even if you have zero accounting background.

Key takeaways

- Good financial reports start with complete and organized transaction data.

- Most businesses only need a few core reports to gain strong financial visibility.

- The value of reports comes from reviewing them regularly and acting on what they show.

What are financial reports?

Financial reports are summaries of your business’s financial activity. They help answer critical questions such as whether the business is making money, where money is being spent, whether there is enough cash available, and whether performance is improving or declining.

In other words, they turn raw transactions into information that owners and managers can actually use.

The 3 most important financial reports

You do not need dozens of reports to get started. For most businesses, three core reports provide the majority of the insight needed to understand financial performance and position.

1. Profit and loss statement (P&L)

A profit and loss statement shows revenue, expenses, and profit over a specific period of time. In simple terms, revenue minus expenses equals profit.

This report matters because it shows whether the business is profitable, helps identify unnecessary costs, and makes it easier to compare performance over time.

2. Cash flow statement

A cash flow statement shows how money moves in and out of the business. It focuses on cash received, cash spent, and the current cash balance.

This report is essential because even profitable businesses can run out of cash. Cash flow reporting helps prevent that by showing actual liquidity, not just accounting profit.

3. Balance sheet

A balance sheet shows what the business owns and what it owes at a specific point in time. Assets include things like cash, inventory, and equipment. Liabilities include loans and payables. Equity represents the owner’s share.

Think of the balance sheet as a snapshot of the company’s financial position at that moment.

Step 1: Record all transactions

Before you can prepare reports, you need reliable data. That means recording sales, expenses, payments received, and payments made.

If your data is incomplete, your reports will be inaccurate. No reporting system can solve missing or inconsistent input.

- Track revenue and sales.

- Record expenses and outgoing payments.

- Capture incoming customer payments and cash movement.

Step 2: Categorize your transactions

Once transactions are recorded, they need to be grouped into meaningful categories. This usually includes revenue, cost of goods, operating expenses, assets, and liabilities.

Categorization makes the reports more organized and more useful. Without it, you only have raw data instead of insight.

- Group sales under revenue.

- Separate operating expenses like rent and salaries.

- Classify assets and liabilities clearly.

Step 3: Calculate totals

Now it is time to summarize the numbers. Calculate total revenue, total expenses, and total cash inflow and outflow.

This is the stage where the bigger picture begins to appear. Totals turn scattered entries into something management can interpret.

- Calculate total revenue.

- Calculate total expenses.

- Summarize cash in and cash out.

Step 4: Generate the reports

Using your categorized data, you can now build the profit and loss statement, cash flow statement, and balance sheet.

This does not have to be manual. Modern accounting and ERP systems can generate these reports instantly, which saves time and reduces reporting errors.

Step 5: Review and understand

Creating reports is only part of the job. Their value comes from using them. Review the numbers and ask practical questions: are we profitable, where are we overspending, do we have enough cash, and are we improving month to month?

Reports are most useful when they directly shape decisions.

Common mistakes to avoid

Many businesses make reporting harder than it needs to be. Common mistakes include waiting until the end of the year, working with incomplete data, not reviewing reports regularly, relying on guesswork instead of numbers, and overcomplicating the reporting process.

The best approach is simple and consistent. Reporting does not need to be dramatic to be effective.

Manual vs automated reporting

Manual reporting through Excel or paper can work for a while, but it is time-consuming, error-prone, hard to update, and limited in insight.

Automated reporting through an accounting or ERP system gives businesses instant reports, real-time data, more accurate calculations, and easier dashboards. Automation saves time and improves quality at the same time.

How often should you prepare reports?

For most businesses, monthly reporting is the minimum. Growing businesses often benefit from weekly reporting, and high-volume operations like FMCG may need daily visibility.

The faster you see your numbers, the faster you can respond to problems and opportunities.

Why financial reports matter for growth

When you understand your reports, you make better business decisions. You can identify profitable areas, cut unnecessary costs, plan expansion more carefully, and reduce financial risk.

That is how businesses move from simply surviving to scaling with more discipline and confidence.

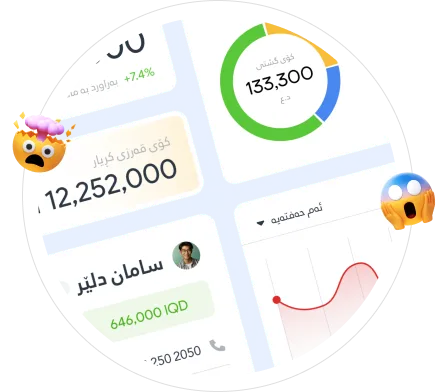

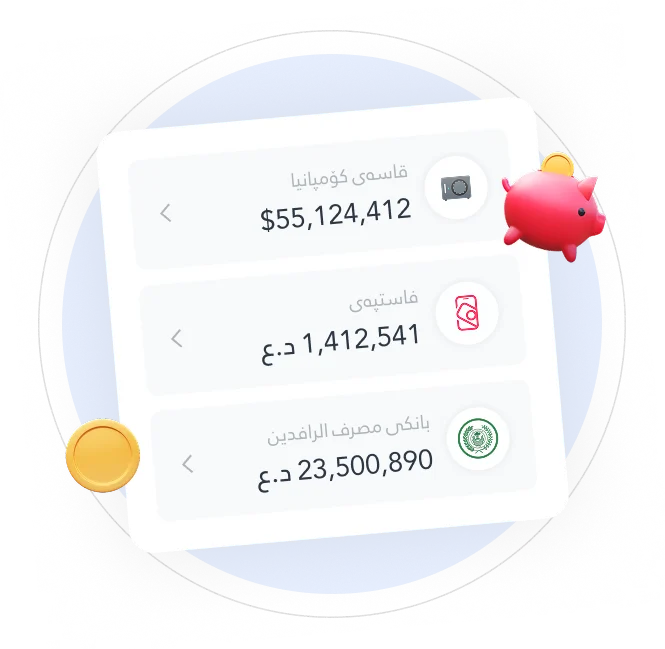

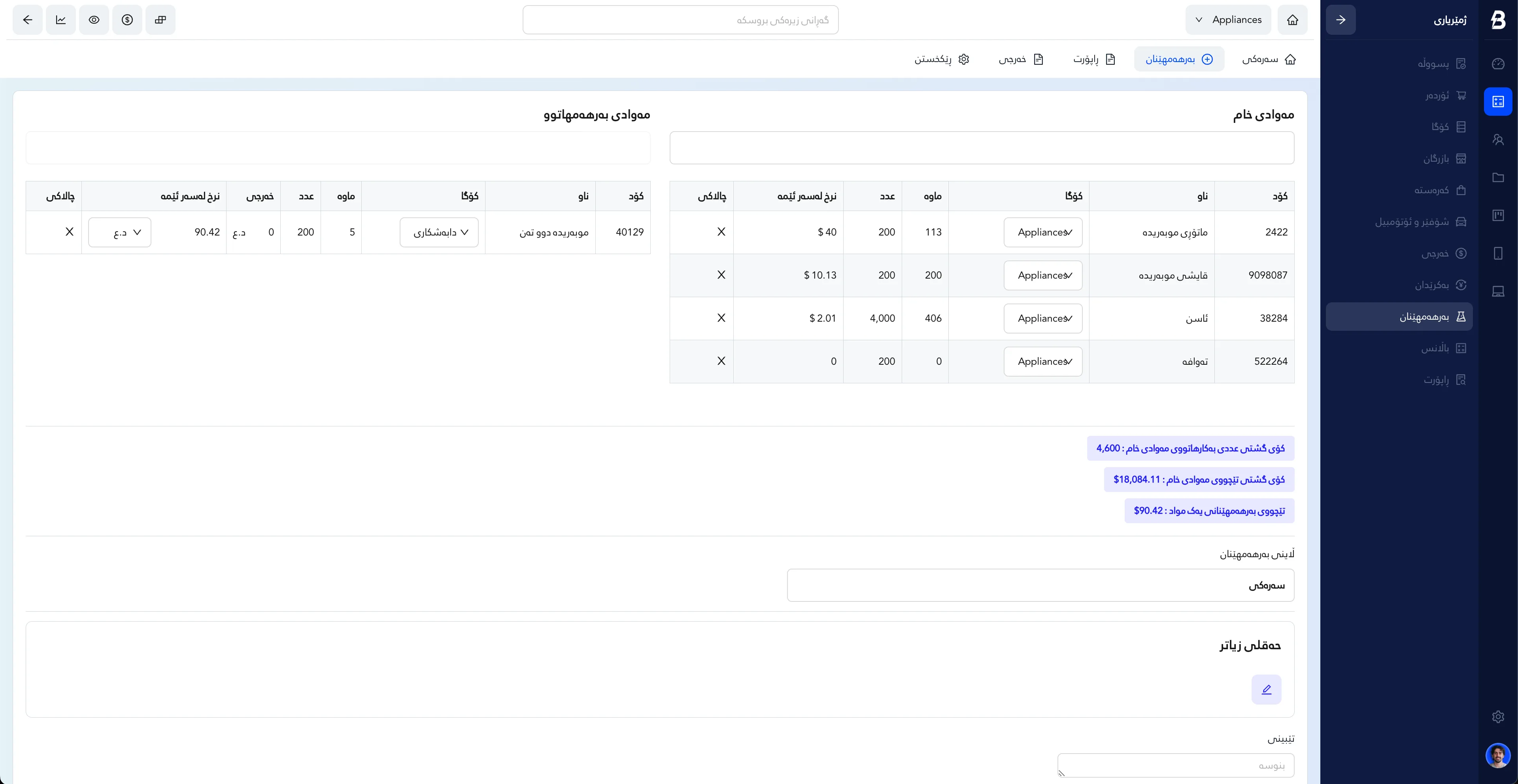

How Bruska makes financial reporting easier

With Bruska ERP, businesses can generate financial reports instantly, track revenue, expenses, and cash flow in real time, and use dashboards that are easier to understand without accounting complexity.

This helps teams move faster and make better decisions without depending on slow manual calculations.

Conclusion

Financial reports are not just for accountants. They are for business owners who want control and clarity. You do not need deep accounting knowledge. You need organized data, a simple structure, consistent tracking, and the habit of reviewing your numbers regularly.

Once that habit is in place, reporting becomes a practical tool for growth, not a technical burden.

Bruska ERP

Bruska ERPMake financial reporting easy

Book a demo with Bruska ERP and see how your business can generate clear financial reports without spreadsheet chaos or accounting complexity.

more than 1,000 companies trust us

More from Bruska

Continue reading

Finance

Cash Flow Management: The Ultimate Guide for Growing Businesses

Growth creates opportunity, but without strong cash flow management it can also create risk. This guide explains how to manage cash flow effectively as your business scales.

Read article

FMCG

Batch & Expiry Tracking for FMCG Businesses

Batch and expiry tracking helps FMCG businesses reduce waste, protect customer trust, and gain better control over stock movement and risk.

Read articleERP

ERP Software for Iraqi FMCG Companies

Learn why Iraqi FMCG companies are adopting ERP software and what features matter most for distribution, inventory, finance, and field operations.

Read article